2020: A Detailed Look

Cambiar President Brian Barish provides an in-depth look at Valuations, Emerging Markets, & the Dollar.

2019 will be an above-average year for stock market returns unless something weird happens next month. Something weird did happen in December 2018, so don’t rule it out completely – there was a technical breakdown in the markets that brought about a derivatives-led selling vortex of -16% in the final month of the calendar year, bottoming on Christmas. So while the S&P 500 is up 25%+ YTD through the end of November (a really good year), it’s up 15% from the end of November 2018 (good, but hardly exceptional). My account of 2018 is that stocks started the year with few risks priced in, but money supply growth in the U.S. was very weak (<4%), which created selling pressure, and the markets had reasons to fear this becoming worse owing to Fed over-tightening. Then some version of shallow markets leading to fragile markets kicked in, as liquidity in the December vortex was never very good. By year-end, a ton of risk was priced in, and as this was reversed in 2019, returns have been elevated. Realize that the trade war stuff had yet to be significantly ratcheted up in late 2018. It got ratcheted up in mid-2019, and markets are up anyway. Pricing, embedded risk, and monetary conditions matter more than the economic outlook.

2020: In the Short-Term

As we enter 2020, stocks in the U.S. look not-dissimilar to how they looked in late 2017/early 2018. They don’t have a lot of risk priced in, and I would argue in the very, very short term, are probably over-bought on trade optimism. Unlike early 2018, the rest of the world remains relatively well-risked with some decent probabilities of positive “surprises” such as a Brexit resolution or relatively better GDP/demand. Also, unlike the end of 2017, we do not have the prospect of an active Fed double-tightening monetary conditions through rate increases and balance sheet shrinkage. The Fed is short-term increasing its balance sheet and will likely not make any moves in 2020. A quiet Fed is a good Fed.

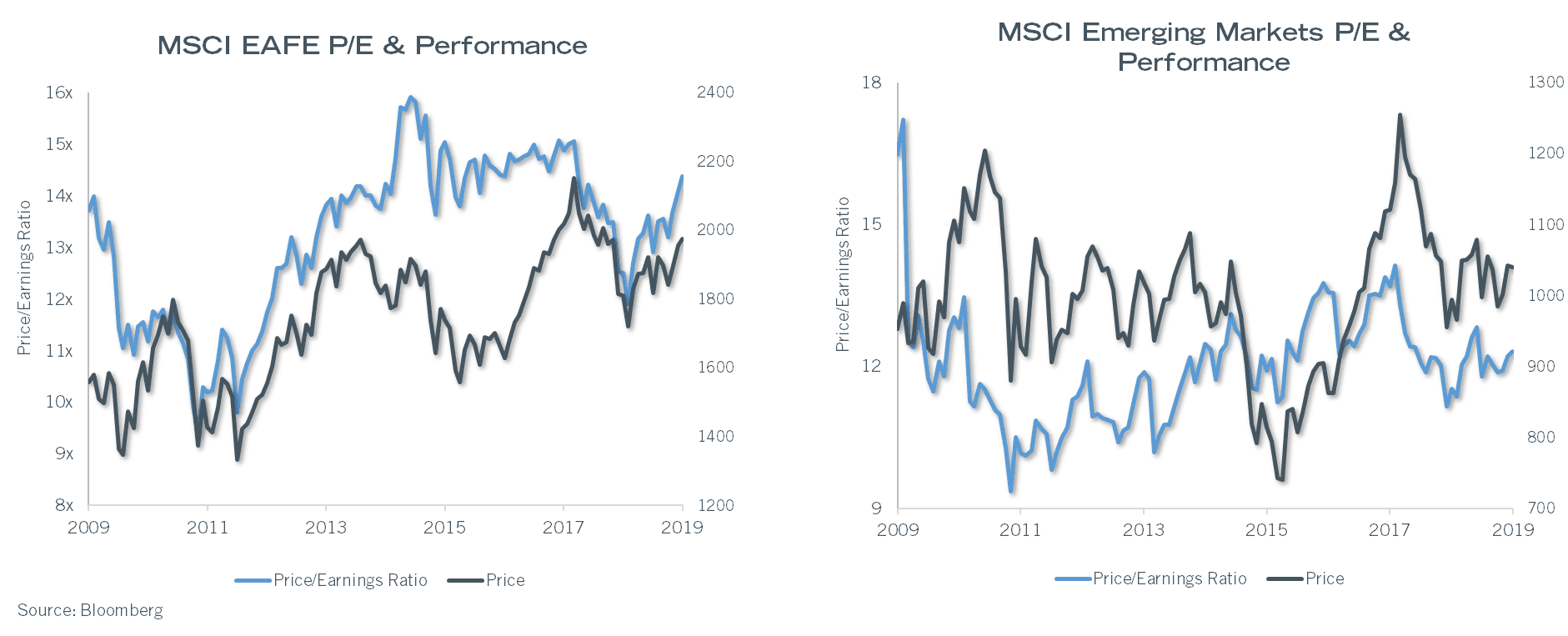

EAFE Index – Does not look nearly as demanding… (some of this is weak currency though).

Emerging Markets Index – Let’s just say thankfully this is not an important product area for Cambiar! There is no return pattern that I see, it just seems to go sideways.

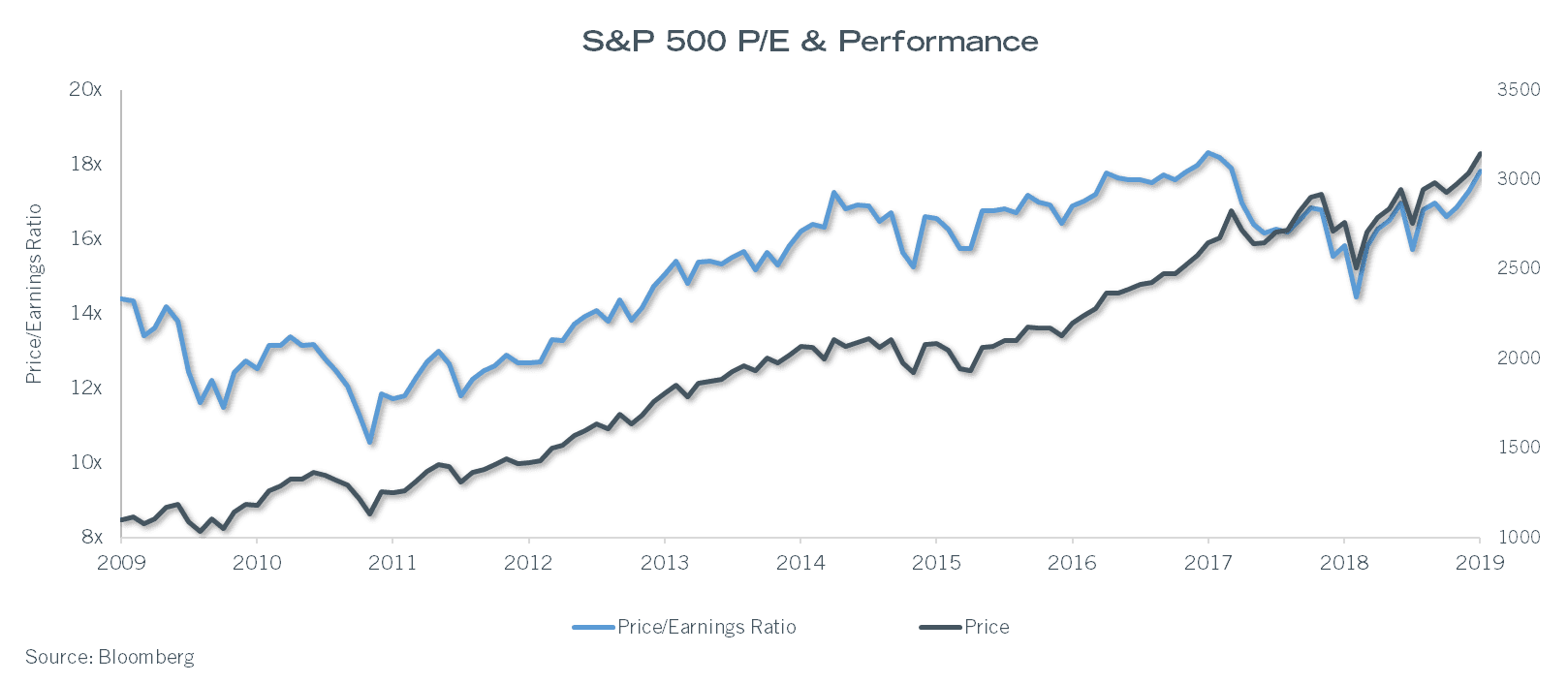

To Summarize – Stock pricing is somewhat demanding in the U.S., less so in the other Developed Markets, but monetary conditions are stable/favorable, as compared to tightening in 2018 and loosening in 2019. Looking at the 1-year forward PE of the U.S., it has not sustained anything over 18x post-GFC, and currently sits at 17.7x. That isn’t a call for sell everything (the market seems to be happy in the 16-17x range). But one would not expect a lot more from here.

For EAFE, the picture is arguably better – EAFE trades at 14.3x forward and seems to top out at 16x.

For the curious, the Emerging Markets index blended multiple sits at 12.3x, which sounds attractive until you look at the LT range. It is similarly about one multiple point way from where it tends to top out. This index really needs to be cleaned up given all the state-related companies that reside in it.

At the end of the 2010s, it is difficult to identify a roadmap to some different version of the world’s strong demand for dollars. Perhaps the best we can hope for is that the U.S.’s current account deficit begins to widen owing to the fiscal side. This… seems possible in the 2020s.

The U.S. has led the world in tech, in financial distress and recoveries, and in novel monetary policies/applications. It seems likely that the U.S. will lead the rest of the world in gigantic structural budget deficits in the 2020s. This is breaking new ground, to have $1 trillion in deficits and unemployment at a 60 year low! There are demographic trends in the U.S. that will almost certainly cause deficits to rise, and politically speaking, the winner of the 2020 election will be a spender, it just depends on who. It is entirely unclear whether deficits of this magnitude are a good thing or an idiotic thing. It does seem to me that the “traditional fiscal conservative” playbook is gone, and the world, for now, needs more/wants more U.S. government debt. Combined with some form of renormalization of monetary policy away from negative rates in Europe, this could lead to all kinds of places. Perhaps the dollar becomes less dominant, or at least more widely available, leading to a weaker dollar versus the 2010s. This would be beneficial on balance for international financial conditions.

IBloomberg

Certain information contained in this communication constitutes “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics/charts may be based upon third party sources that are deemed reliable; however, Cambiar does not guarantee its accuracy or completeness. As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that any opinions expressed herein will be valid beyond the date of this communication.