The Last Dance For The Traditional Customer Approach

We examine the acceleration of digital economy businesses during this pandemic.

The Torch Has Been Passed…

There has been no greater excitement for me after having spent two months in confinement than getting to watch The Last Dance docuseries on ESPN about the 1990s Chicago Bulls team. The most epic moment for me by far was watching the Chicago Bulls beat the Bad Boys Detroit Pistons team in the 1991 Eastern Conference Finals. Until then, Detroit was our biggest rivalry as the Bulls lost to them the prior 3 years in a row during the playoffs. As a kid born and raised in Chicago, those losses to the Pistons were gut wrenching. But beating them in 1991 for the first time was a breakthrough moment for the team and the highlight of my 13 year old life at the time. They then went on to beat the Lakers in the Championship and in the words of Magic Johnson, “The torch had been passed.”

Watching the Bulls win the Championship ring in 1991, many basketball fans at the time (including yours truly) felt that they were witnessing the beginning of a new era of leadership. As I am writing this update while waiting for our Uber Eats driver to deliver dinner for the night, I can’t help but think that this Covid-19 crisis is likewise going to bring about a new era for many companies – with some getting better and stronger over time at the expense of various weaker players. This pandemic has given the global investment community a glimpse into the future for many industries, as trends that would’ve normally taken 5-10 years to play out are happening in the span of a few short months. If there were any doubts as to how the digital economy would hold up during tough times, this crisis should remove most of them.

Anecdotes from recent earnings reports via a number of digital economy companies held across Cambiar’s portfolios as of March 31, 2020:

Delivery Hero (European food delivery company owned by Cambiar holding Prosus) added a record 50,000 new restaurants to its food delivery network in the last three weeks of March alone

Delivery Hero (European food delivery company owned by Cambiar holding Prosus) added a record 50,000 new restaurants to its food delivery network in the last three weeks of March alone- Enterprise software company SAP reported a 24% growth in its future cloud bookings from clients during their first quarter despite Covid-19 shutdowns

- Tencent (30% owned by Cambiar holding Prosus) reported a 31% growth in its gaming revenues, 32% growth in online advertising revenues, 26% growth in online video subscriptions and a 50% growth in streaming music subscriptions

- Amazon reported 29% revenue growth across its North American retail division and 33% growth Across its AWS/cloud platform

- Alphabet reported revenue growth of 13% with 55% growth in cloud revenues

- IT Services provider Cap Gemini reported 20% growth in revenues for its cloud and digital transformation revenues

- Ahold (European listed grocery chain) saw online grocery sales grow 38% y/y due to country wide lockdowns

Interesting anecdotes from digital economy companies we don’t own…

- Peloton saw its digital subscribers to its fitness app jump 66% in the first quarter as consumers worked out at home

- Netflix added nearly 16 million net new subscribers in the quarter, nearly double expectations

- Microsoft Teams had more than 200 million meeting participants in a single day in April. It now has more than 75 million daily active users globally, double the number pre-Covid-19

- Uber Eats recorded a 54% increase in gross bookings for food delivery as consumers sheltered in place

- Disney’s on demand video platform Disney+ saw the number of subscribers on its platform grow 65% quarter over quarter to nearly 55 million

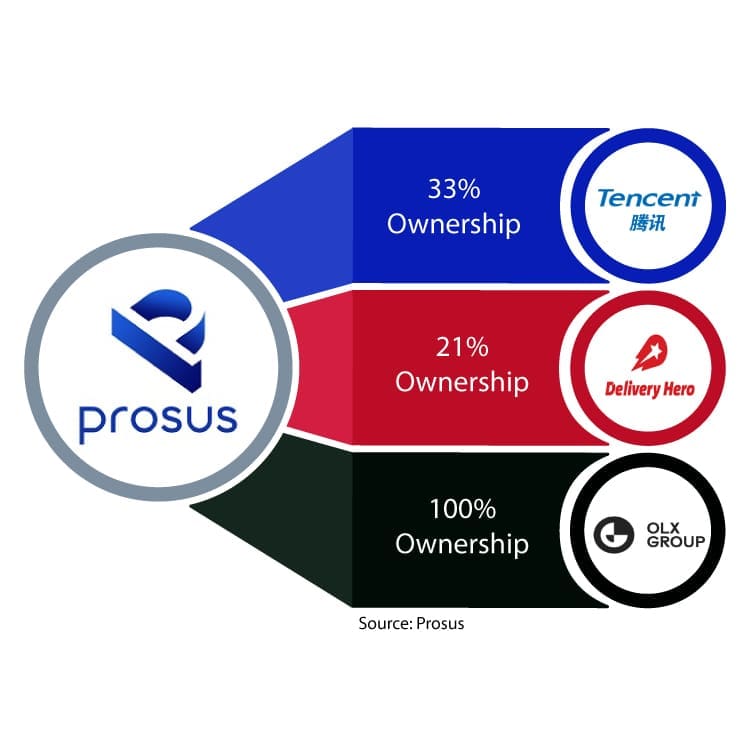

As investors first and foremost, Cambiar prefers to own what we believe are advantaged businesses rather than the opposite. Owning structurally advantaged companies is a key part of our investment philosophy. Take for example two of our holdings Prosus and Alibaba. Prosus, listed in Amsterdam, and trades for €69 per share (as of 4/30/20). Prosus, in our view, owns and manages some of the most attractive digital assets in the world while trading at a price that is entirely inconsistent with the underlying value of those assets. The company owns a 33% stake in Tencent worth €104 per share currently. Tencent is one of the most innovative and dominant online platforms in the world. Tencent is the largest gaming company on the planet with 50% market share in China alone. Tencent’s mobile payment wallet called WeChatPay is a duopoly and second only to Alipay (owned by Alibaba) in the country. The company has a fast growing online advertising business and the second largest cloud platform in China. The company’s music platform is the leading streaming music service in the country and Tencent video is now challenging for pole position in terms of online video streams. Furthermore, Prosus’ current online classified segment called OLX is conservatively worth another €10 per share. In addition Prosus owns a 20% stake in Delivery Hero, a fast growing and well positioned European food delivery platform worth €3 per share. Finally Prosus is sitting on another €4 per share in net cash. All in this is a business whose stock we think is conservatively worth much more than its current share price implies.

As investors first and foremost, Cambiar prefers to own what we believe are advantaged businesses rather than the opposite. Owning structurally advantaged companies is a key part of our investment philosophy. Take for example two of our holdings Prosus and Alibaba. Prosus, listed in Amsterdam, and trades for €69 per share (as of 4/30/20). Prosus, in our view, owns and manages some of the most attractive digital assets in the world while trading at a price that is entirely inconsistent with the underlying value of those assets. The company owns a 33% stake in Tencent worth €104 per share currently. Tencent is one of the most innovative and dominant online platforms in the world. Tencent is the largest gaming company on the planet with 50% market share in China alone. Tencent’s mobile payment wallet called WeChatPay is a duopoly and second only to Alipay (owned by Alibaba) in the country. The company has a fast growing online advertising business and the second largest cloud platform in China. The company’s music platform is the leading streaming music service in the country and Tencent video is now challenging for pole position in terms of online video streams. Furthermore, Prosus’ current online classified segment called OLX is conservatively worth another €10 per share. In addition Prosus owns a 20% stake in Delivery Hero, a fast growing and well positioned European food delivery platform worth €3 per share. Finally Prosus is sitting on another €4 per share in net cash. All in this is a business whose stock we think is conservatively worth much more than its current share price implies.

Alibaba is the dominant e-commerce marketplace, cloud infrastructure provider and mobile wallet platform in China. Cambiar purchased Alibaba during the recent crisis. Alibaba’s share price and market cap has remained largely flat since 2017, despite earnings for the company – almost more than doubling (through year-end 2020). As a consequence, at the current price of $203 per share (as of 4/30/20), we believe we get to own Alibaba’s core e-commerce marketplace at a historically depressed valuation, while receiving the company’s dominant cloud infrastructure and payments platforms essentially for free. Alibaba’s e-commerce marketplaces (called Taobao and TMall) have a combined 960 million annual active users and deliver 57 million packages a DAY. 60% of all products purchased online in China go through the Alibaba marketplaces. Alibaba’s cloud platform (called AliCloud) commands 45% market share in cloud infrastructure services in China, larger than the next four players combined. AliCloud generated roughly $5 billion in revenues in 2019, and we think it can easily double over the next 2-3 years. It is important to highlight that AliCloud was just a fraction of itself a few years ago. In addition, Alibaba’s payments brand (Alipay) was valued last year at around a $150 billion market cap; this is effectively one of the largest privately held companies in the world, akin to PayPal, but exposed almost entirely to China. Alipay accounts for 55% of all mobile payments in China. In our estimation, these two free options (AliCloud and Alipay) are worth somewhere between $40-$50 per share relative to Alibaba’s current share price of $200. All in, we believe Alibaba’s current share price meaningfully ignores the underlying intrinsic value of this company.