Market Insights – 2Q19

Cambiar President Brian Barish provides his latest thoughts on the fixed income environment, China, and that 90s feeling.

Global equity markets generated modestly positive performance in the second quarter of 2019, following a vigorous across-the-board gain earlier in the year. U.S. large-cap stocks gained about 4% in the quarter, while international stocks as measured by the MSCI EAFE index posted a similar return (in U.S. $ terms). U.S. small-cap stocks (as measured by the Russell 2000 Index) gained about 2%. Emerging market stocks generated a flat return for the quarter.

Many stocks experienced their peak prices early in the quarter, but then stumbled in May as trade friction between the U.S. and China pierced an otherwise cheerful tape. Following a positive tone to a G20 economic summit in Asia in early June, suggestive of some desire to “get a trade deal done”, stock prices then recovered closer to April highs. The late-quarter recovery was more heavily skewed to defensive, bond-proxy, and growth stock names, with more cyclically geared businesses such as industrials, commodities, and financials lagging the broader markets.

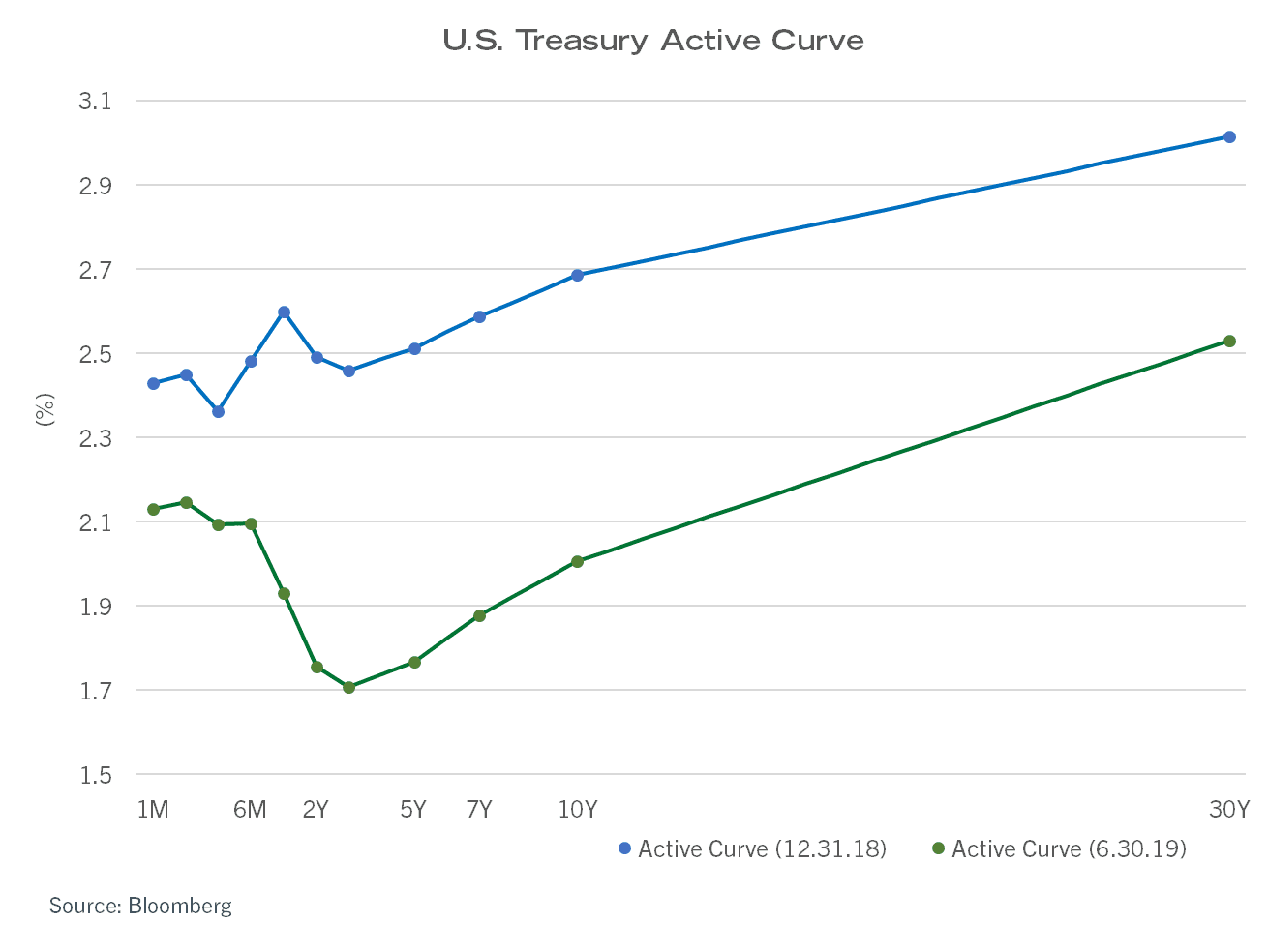

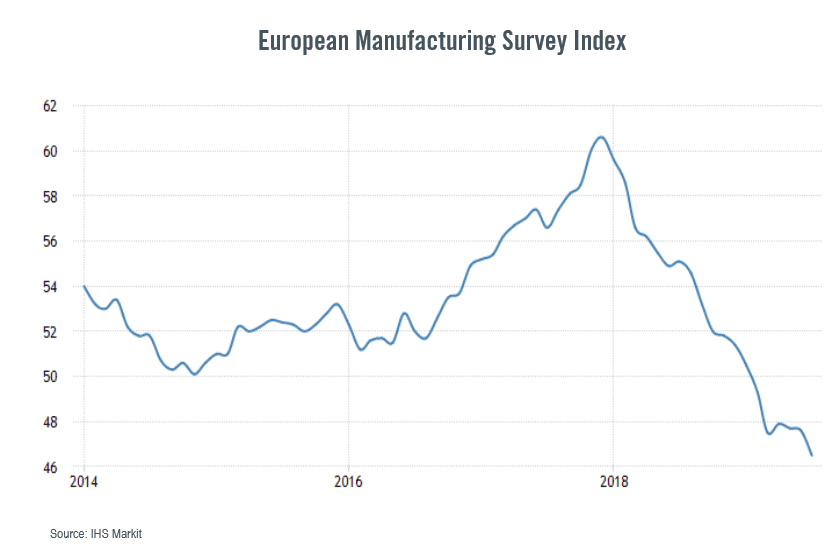

The more confrontational trade tone arrived on the back of generally weak economic figures emanating from China and Europe, along with some slowing in U.S. leading indicators. The slowdown in economic growth measures led bond yields sharply lower. The U.S. yield curve had partially inverted in March; however, it went into a more complete inversion in May, and has remained inverted across most combinations of maturities. There are 44 possible combinations of yield spreads between the overnight rate all the way out to 30-year bonds. Approximately 60% of these combinations had inverted by mid-quarter, a level that has consistently been a signal of oncoming recessionary forces within the next 12-24 months. Outside the U.S., yield curve inversions are nearly impossible to achieve due to the use of negative deposit rates at the ECB and the Bank of Japan. However, longer duration instruments can and have yielded negatively as a sign of discomfort with the business outlook. This peaked in 2016 at approximately $12 trillion of bonds around the time of the Brexit vote in June 2016. By mid-second quarter, something in the range of $14-15 trillion worth of sovereign bonds were yielding negatively, mostly in Europe, as the market priced in the possibility of ever-lower ECB deposit rates.

(values >50 = expansion, <50 = contraction)

European Industrial Activity has slowed to the point of contraction…

…pulling German bond yields deep into negative territory.

This is a new record low for German bond yields!

Despite the ominous vote of no confidence in medium-term economic vitality or the achievability of inflationary goals, stocks have held up remarkably well (so far). A changed tone by the U.S. Federal Reserve suggests the last two rate hikes of 2018 would probably be reversed in 2019. This would bring short term rates back down below 2.0% and would end the balance sheet roll-off of assets accumulated during the multiple rounds of quantitative easing in 2009-2015.

With rates poised to go lower and erode fixed income return potential, the thinking can be summed up in an acronym, TINA, or “there is no alternative” to stocks to generate portfolio returns. Stock market P/E multiples, which briefly hit the 14x level in the U.S. in December and the 11x level in Europe, have bounced by three and two multiple points, respectively, in 2019. Growth-cyclical areas of the market such as semiconductors and higher value-added industrial products have performed considerably better than the averages, though defensive and core growth names have also performed well. Economically-sensitive businesses such as banks, chemicals, autos, and materials continue to struggle. For many of these companies, earnings are not necessarily so poor as investors’ collective comfort in their sustainability – though there are genuine signs in the markets that global demand for “big physical stuff” such as bulk chemicals is tracking south. The split between stock valuations of companies benefiting from longer-term growth trends in their specific areas of business, versus the slower lane, is stark. Though aggregate market multiples as of June 2019 are unremarkable versus longer-term history, the spread between the richer and the poorer valuations is particularly stark.

Whether part of the TINA psychology or just a feature of overconfidence in a market that has been going up for a long while, there is an increasingly large cadre of what one could loosely call “concept stocks” trading at exorbitant valuations; current examples include leading-edge software, payments, and synthetic foods. Ironically, two of the biggest concept stock IPOs of the last few years, ride-sharing leaders Uber and Lyft, IPO’d in the quarter and immediately shed tens of $ billions in valuation, suggesting a degree of speculative fluff to this phenomenon.

It Does Feel a Lot Like the Late 1990s Out There…

Where markets go from here is difficult to say, but the TINA and speculative mentalities that pervade these larger pockets of the markets are worrisome signs. At a very high level, the global economy depends too much for growth on the large economies of the United States and China, as developed Asia and Europe are unable to develop much self-sustained internal growth. Trump’s trade tension escalation was uniquely well-timed – seemingly by accident – with efforts by China to crack down on credit growth in informal channels, leading to sharply reduced demand for consumer and capital goods and diminished consumer confidence. China is no longer an ideal country in which to outsource labor-intensive production (wages are closing in on European levels) and as a wealthier country, its appetite for imports has grown, leading to a roughly balanced trade account presently. China is still very much an emerging market – just a very large one, and emerging market financial systems are extremely dependent on their capacity to generate and sustain foreign reserves. With Chinese manufacturers facing tariffs (or outright bans in some cases), their terms of trade are notably worse, and their economy will be challenged to grow at all should reserves deplete. Chinese manufacturing jobs are in decline from both cost pressures and the chilling effect of the tariff threat. Over 4% of the country’s factory workers have lost their jobs since early 2018 (roughly 8 million workers) (source: Credit Suisse), and China does not have much of a social safety net. That creates a lot of internal pressure on an unelected government. It is more likely than not that the Renminbi will need to trade lower to compensate for these factors.

Internally, the Cambiar Research Team is not of a singular mind as to whether a couple of Fed tweaks downward in interest rates can extend the now-long U.S. economic expansion even further. This happened once (successfully) in the mid-1990s, but no yield curve inversion was observed at that time, and the Fed’s titrating adjustments came barely halfway through the economic cycle. Thus some skepticism as to pulling this feat off today. On the other hand, business profitability is high and the monthly statistics on unfilled job openings remain stratospheric versus other business cycles. There is tremendous demand for workers at many levels of skill.

As business cycles end, unsustainable relationships between asset prices and underlying fundamentals are exposed, leading to wealth destruction in these pockets of the market. Prior to the 2001 recession, it was reasonably obvious that technology and internet stocks had become divorced from near-term earning power. Similarly, residential housing prices had become untethered from disposable income trends leading up to the 2007-09 recession. The result in both cases was a sharp decline in value, although the circumstances in the 2007-09 timeframe were much graver because of all the private credit that needed to be marked down and restructured alongside the overvalued homes. As the yield curve inversion presents a clear warning signal, can we identify the unsustainable relationship and potential collateral damage?

We are opting for portfolio balance in most investment strategies, striking a balance of exposures that is neither overtly cyclical nor intentionally defensive.

There don’t seem to be a lot of obvious bubble-sectors in the economy that need recessing. Corporate leverage is statistically elevated, though the cost of servicing debt remains paltry due to the chronic low rate regime that has prevailed this decade. There is an uncomfortably large amount of low investment-grade rated debt (BBB to BBB-) in fairly heavily leveraged companies, and at least a few of these situations are bound not to work out so favorably, leading to some disruption potential should these debts be downgraded to junk status. The junk bond market is much smaller than the investment-grade market, and by our reckoning would have a difficult time suddenly absorbing a huge influx of paper. We are not overly confident that commercial real estate values will hold up, as the internet revolution has de-coupled the normal relationship between location and real estate value. If the economy and consumer confidence were to contract, we suspect various advertising-led businesses could prove not to be the secular growth stories their investors expect them to be. Other large industries such as energy and autos seem bound to morph into very different versions of themselves over the next decade. It is entirely possible that the bubble lies in our collective confidence in central bankers to apply the correct medicine when that is just another heavy dose of lower interest rates. This kind of therapy isn’t working particularly well in Europe or Japan, and ultimately leads to greater asset price distortions – exhibit A is the trillions in negative-yielding debt. Our last two recessions were mostly caused by asset bubbles than a specific need to crimp spiraling inflationary pressures…

For now, we are opting for portfolio balance in most investment strategies, striking a balance of exposures that is neither overtly cyclical nor intentionally defensive. We are also being a bit stricter than usual with respect to price targets.

In the initial drafting of this letter, my plan was to discuss a handful of stocks and their respective stories. But there’s one name, Anadarko Petroleum, an evil demon of a stock if there ever could be such a thing, whose final exit from the stock market and Cambiar portfolios in 2019 provides quite a commentary on this whole decade. Importantly, while we salvaged some return from this position in 2019, this position was not a winner for Cambiar, certainly not on a long-run or risk-adjusted basis. Rather, it was a great opportunity cost versus many possible investment alternatives. The energy space is ultimately a story of change, both in terms of the energy market and investors’ willingness to accept or not to accept certain kinds of risks, as the prevailing thinking about what constitutes value in energy has evolved significantly. It is also a comment on ourselves and how we have evolved the internal thinking at Cambiar over the last couple of years.

Anadarko is emblematic of the deep changes in the energy market that have taken place over the past 15 years. Going back to the mid-2000s, Anadarko was particularly well regarded in terms of geological skill, and the company built an impressive portfolio of oil finds in North America and abroad. Anadarko found several massive oil deposits in the Gulf of Mexico and a truly world-class giant gas deposit in Mozambique. The company also possesses large holdings of drillable acreage in Colorado and the Permian Basin in Texas. This collection of assets constituted a unique treasure trove of potential reserves that many investors, including ourselves, reasoned one of the major integrated oil companies would want to add to its portfolio at some point in time. That was back in the 2000s, the pre-iPhone era, and a time when almost everyone was convinced that the future demand for hydrocarbons from populous emerging markets such as China and India meant persistent future supply challenges. Exploration skill and producible fields were highly prized.

Cambiar’s first investment in the stock was in 2007, and Anadarko became a volatile (though outperforming) holding for about seven years. An almost impossible-to-fathom series of wholly unanticipatable market developments provided a number of opportunities to selectively add to or sell parts of the position profitably:

- Anadarko’s stock price roughly doubled in the commodity bubble of early 2008,

- collapsed by 70% in the peak financial crisis period in late 2008 (where we bought more) and then proceeded to return to 2008 highs in 2009-10,

- somehow managed to be a minority stakeholder in the ill-fated BP Deepwater Horizon drilling accident, creating a buying opportunity after a 50% loss,

- rallied again sharply in 2011-13 by 150% as the market repriced upward the prospects of their North American shale position and the massive gas discoveries in Mozambique,

- only to fall 30% owing to a litigation issue from an old acquisition in late 2013, which created another opportunity after the market over-estimated the associated liability.

The stock peaked at over $110 in early 2014 after this liability issue was decisively put to bed, up almost 3x from the 2007 purchase and with some generally successful interim trading in the multitude of near heart attack producing moments.

At that point, we should have walked away from Anadarko – and anything else to do with upstream energy.

The North American oil and gas shale boom was beginning to show it could scale far beyond initial expectations, a development that has proceeded to wreck the structure of the oil market. For decades, energy, and oil specifically, constituted a “strategic anomaly” commodity – absolutely essential to mature and developing economies, with low price elasticity, and only found in material producible quantities in a few places around the globe. New discoveries happened in non-OPEC countries, but often tended to take immense amounts of time and capital to bring to the markets. Incremental supply was long-cycle. All of these conditions changed with shale. Incremental supply could be brought to production quickly, and North American producers proved adept at lowering unit costs continuously. OPEC sensed a threat in late 2014, and reached for a proven play from their playbook – i.e., a short-term supply flood to crush pricing and snuff out new projects. In the 2000s, this ploy would have worked beautifully, but not in the 2010s. Shale production rebounded rapidly within months of OPEC production restraint in 2016. Today, despite the (unanticipated) loss of millions of barrels of production in Venezuela and (also unanticipated) loss of millions of barrels of Iranian oil due to U.S.-led sanctions, oil markets teeter on oversupply because the shale production and efficiencies just keep coming.

In early 2016, we made a grave error and capitulated on our Anadarko position, rationalizing that their vast portfolio of assets probably wasn’t so valuable with the world in chronic oversupply, and not really in need of new oil finds. We exited the position. The reasoning behind the move is perhaps entirely accurate today, but the timing on the Anadarko sale looked awful. A changed regime in Saudi Arabia and new partnership between Russia and OPEC restored stability to the global oil market very shortly after our sale. Energy stocks bottomed in early 2016, and performed well over the balance of 2016 as North American shale production did indeed decline, though it took oil prices in the $20s per barrel to crush drilling activity. Cambiar re-established positions in various other upstream energy companies over the course of 2016-17 on the thesis of improved and fiscally necessary stewardship of the energy market. In late 2016, we added a position in a smaller but similar shale and offshore producer called Noble Energy, unwilling to re-attach to Anadarko. That one was just too wild to ride again.

Fast forward to late 2018, and energy producers are yet again sliding as a super-tight oil market is roiled by the market’s collective inability to properly read the Trump administration’s plans regarding Iranian oil sanctions. The Saudis inadvertently flood the market to sustain a supply cushion for an Iranian embargo that does not fully materialize. Cambiar’s position in Noble Energy falls more than most, as the company (along with Anadarko) is a big producer in our home state of Colorado. An aggressively worded November 2018 Colorado State ballot included an initiative that would greatly expand drilling setbacks – if passed, the initiative would effectively ban most drilling activity, thereby devaluing Noble and Anadarko’s respective positions. By our calculations, the stocks jointly lost the value of the drilling potential a couple of times over during the selloff, with Anadarko plunging back close to the levels at which we had sold it in 2016. On the ground in Denver, a generally ecologically sensitive city, we did not detect much broad support for the initiative and thought the two stocks’ selloff was not rational. Wearing a material loss on Noble, we thought there was a chance to atone for the error a few years back and generate a tax loss while at it, thus a decision was made to swap out of Noble and back into Anadarko. Given the astonishing number of elevator rides as an investor in Anadarko, I privately wondered if I needed to seek some form of psychological evaluation.

After an initial post-election bounce (the ballot initiative failed decisively), Anadarko stock went nowhere for the next few months. We barely recovered any of the loss in Noble despite what seemed like a clever swap.

By late 2018, Cambiar’s house view on energy had been thoroughly re-examined. We concluded that the improved stewardship of the global supply of oil by ROPEC (that’s Russia plus OPEC) was mostly luck, and the poor structure of the industry (shale efficiency leading to chronic oversupply, along with the eventuality of electric cars bending down demand permanently) was eventually bound to render the physical market unmanageable. Cambiar began shedding production-oriented stocks across our different investment strategies. Anadarko was definitely on the chopping block as well, but even armed with a much gloomier view of the medium-term oil price, the stock still seemed distinctly undervalued.

In April 2019, deliverance finally arrived. A takeout bid for Anadarko by Chevron at a large premium to the market price, though this was not a much better price versus where the stock had traded just 8 months earlier. Anadarko management apparently did not disagree with our gloomy assessment of the energy market (or their ability to sustain a reasonable stock market valuation), and was happy to take a bid in the $60s per share. In happier times, Anadarko probably would have merited $100+, but those days are long gone. Energy investors don’t want exploration success or greenfield projects with lots of upfront investment costs. They just want their money back, a challenging proposition for exploration and production companies to deliver on. Occidental Petroleum, had also been a suitor, and proceeded to raise the bid and ultimately win Anadarko in the low $70s. However, in so doing, managed to utterly sully their reputation for financial prudence and discipline.

The energy sector today has dwindled to less than 5% of overall stock market capitalization, down over 80% from 2008 levels in the mid 20% range, with much of what’s left dominated by big integrated oil companies. Key sub-sectors, such as oilfield services and drilling companies, are now heavily populated with microcap and penny stocks that had been large and mid-cap stocks just a few years ago. From a stock market perspective, upstream energy resembles Afghanistan, not west Texas. In our large-cap strategy, we still hold positions in an integrated producer, Chevron, and ConocoPhillips, a low-cost production-oriented company, while in our International strategy the positioning has been confined to integrated oils for some time. Within Cambiar’s smaller-cap strategies, we view the risks to capital loss to be too high, and subsequently have very low exposure to energy companies. There may be some reasonable investment opportunities downstream in refining and infrastructure companies.

The well-managed energy companies that operate in the current market one – and only one – demand from shareholders who are still willing to maintain a position in the sector: return capital. Dividends and buybacks are welcome. No, don’t upsize your drilling budget. No, don’t acquire somebody else for the sake of “scale”. Just send us the checks please! It’s a far, far cry from the Malthusian fears that drove oil prices to the $140 per barrel peak in mid-2008 and led investors to value geological potential at exorbitant prices. In a chronically oversupplied market that may soon prove difficult for its historic handlers to manipulate profitably, investors understandably just want their money back. Had the technology to produce oil from tight shales not been developed and not proven so scalable, these Malthusian fears would have held more merit, and offshore production titans such as Petrobras might today rival the internet platform giants for the world’s biggest market cap. But shale technologies were developed, continue to scale, and it does not appear as though creative new sources of supply are really going to be needed – particularly in light of high development costs and long lead times that accompany such projects. From the perspective of “how are these stocks supposed to work”, in our opinion it would seem that not many can, as the wildcatter mindset predominates in energy management.

Internally at Cambiar, we have historically looked for catalysts to drive stock price appreciation.

Internally at Cambiar, we have historically looked for catalysts to drive stock price appreciation. Catalysts can take many forms, often some discrete event or combination of events and associated financial performance, that would lead other investors to potentially take note of the company in question. Given its many exploratory activities and global oilfield holdings, a stock like Anadarko was a veritable treasure trove of possible catalysts when looked at this way. Yet our cumulative returns were poor. In part, we did not recognize the impact that shale would have on market structure early enough, rationalizing that it was mostly a high-cost form of energy in the early 2010s. A missed call to be sure. But secondly, whether high cost or a rapidly-decreasing cost form of energy, the underlying economics were bound to be poor, featuring high reinvestment rates to grow production and challenges in valuing the underlying assets because of these features. E&Ps either grow and consume capital, or stop growing and generate capital, but even careful capital stewardship leads to questionable sustainably if other producers are going full throttle. We have shifted our internal discourse to thinking about an “alpha thesis” for stocks being contemplated for the portfolios. It’s certainly a similar process as looking for catalysts, but we are layering in a much more thoughtful appraisal of the underlying business characteristics. The underlying business characteristics of an E&P are challenging to begin with. Add on the poor market structure that has enveloped the energy space and – how exactly can you generate good returns over the long haul? Why exactly is a richer valuation warranted? Indeed, if the main measure that investors care about is whether they can remove capital generated from the sector, how is this good? The alpha thesis would appear lacking, catalysts though there may be. We have been implementing this change in mindset across portfolios in the past several quarters, with increasingly evident benefits. It’s a good philosophy with respect to stock screening.

Epilogue

Certain information contained in this communication constitutes “forward-looking statements”, which are based on Cambiar’s beliefs, as well as certain assumptions concerning future events, using information currently available to Cambiar. Due to market risk and uncertainties, actual events, results or performance may differ materially from that reflected or contemplated in such forward-looking statements. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or endorsement to buy or sell any security, investment or portfolio allocation.

Any characteristics included are for illustrative purposes and accordingly, no assumptions or comparisons should be made based upon these ratios. Statistics/charts may be based upon third party sources that are deemed reliable; however, Cambiar does not guarantee its accuracy or completeness. As with any investments, there are risks to be considered. Past performance is no indication of future results. All material is provided for informational purposes only and there is no guarantee that any opinions expressed herein will be valid beyond the date of this communication.